5 Credit Card Mistakes That Destroy Your CIBIL Score

-

- July 02nd, 2026

- 35 views

FREE SEO Topical Map Generator: Find Your Next Content Ideas

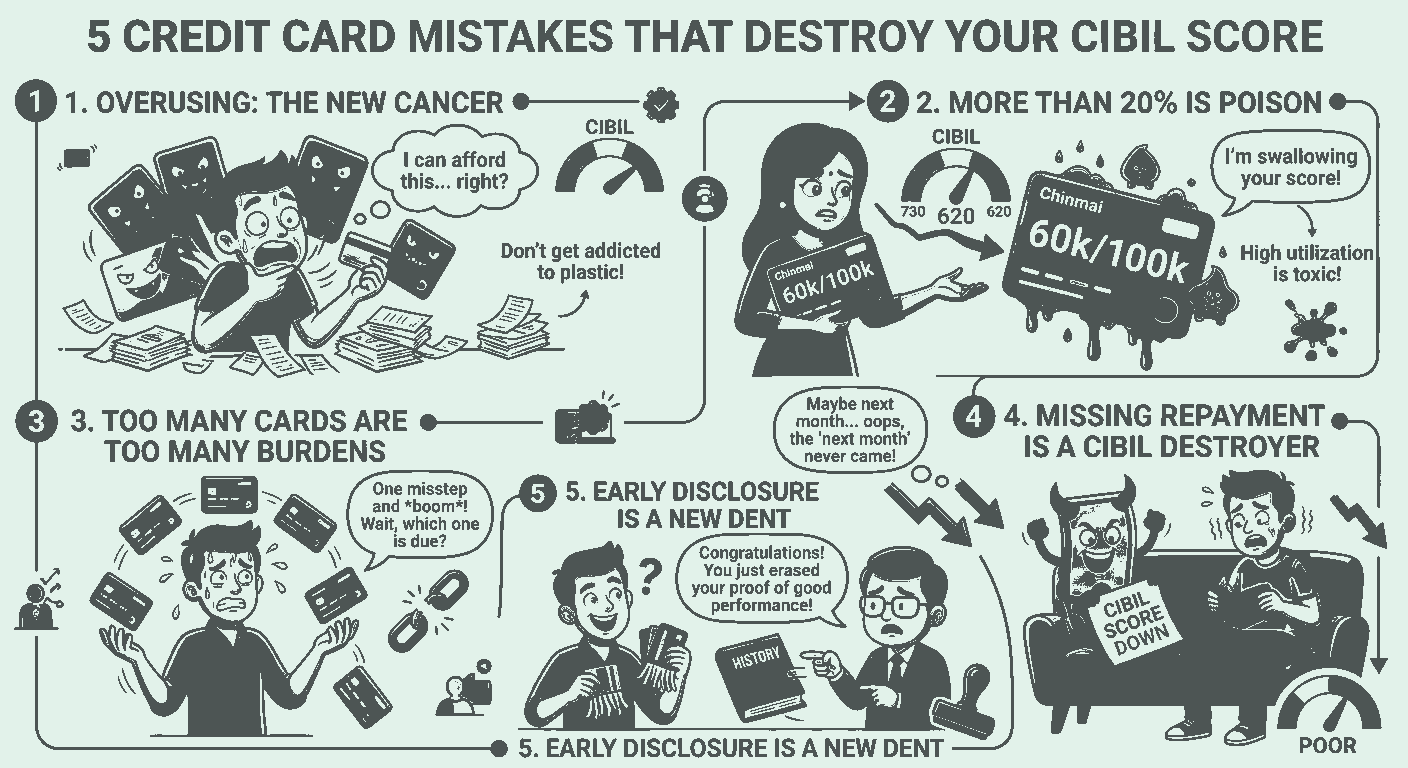

Overusing is the new cancer

A credit card is the favourite topic for people when it comes to personal loans or personal expenses. Sometimes this overexcitement leads to something that nobody wants in their financial health. It is just like how overeating leads to your physical health.

Overusing credit cards is also like an addiction for your financial health. Just like how smoking becomes an addiction to people, leading to cancer. It will not affect you physically, but financially. When you overspend from your credit card directly, you're burdening yourself with too many interest rates at high interest rates.

The higher the interest rate, means a higher the financial burden. This will destroy the CIBIL score.

More than 20% is a poison

Imagine you have a credit card limit of 1,00,000 rupees. Human psychology says you have more money to use now, so use it. So, many people just blindly use the money.

Chinmai did the same thing; she used 60,000 rupees from her 1,00,000 rupee credit card limit. And this was a recurring activity from her side. She never realised she was almost using more than 50% of her credit capacity. This risked her CIBIL score, and she ended up with too many debts and too much interest.

Chinmais’ credit score dropped like melted ice cream, straight from 730 to 620. This was not the instant action, but he was overusing his credit card by more than 20%, which led to this result.

Too many credit cards are too many burdens

Flexing too many credit cards is not really smart, but handling too many credit cards is the real smartness. Many people often buy credit cards for more use without realisation.

One never realises that it will increase their financial burden, repayment structure, and interest rates. One miss, and their credit score boomed. A single repayment miss will lead to a huge credit score gap that will take more than 3 months to recover without conformity.

Buying multiple credit cards also needs a smart strategy to tackle this financial burden. One needs to understand that until it is a need, buying a credit card is no longer a luxury. Larger amounts are bigger loans, which definitely need a better approach and strategy, which is where many people go wrong and mess up their credit score permanently.

Missing repayment is a CIBIL destroyer

Many times, it happens that people use credit cards to their full limit but forget that regular repayment is necessary.

We tend to always push to next month's EMIs. “Aj paise nai hain; next month bhardenge."

The "bardenge" never comes. This is what people often do wrong. Imagine you use the credit card for about 40%, which is 40,000 rupees from the 1,00,000 credit limit. Obviously, it is more than 20%; even if you paid regularly, you would have saved yourself, but the case was totally opposite. You missed your repayment of 1,800 monthly. Struggling to manage multiple loan EMIs? Explore Debt Consolidation to combine your existing loans into a single, easy-to-manage monthly payment. https://www.loansjagat.com/debt-consolidation-loan

Your missed payment led to the score burden, which eventually dropped day by day. Underestimating repayments makes it always difficult to balance the EMIs and interest rates to increase the CIBIL score.

That is why it is said, "What's the use of crying over spilt milk?'

Early disclosure of credit cards is a new dent

We often think that a closed credit card, which is fully used and cleared, is a new trend. People forget that their credit history counts, and if they have performed excellently in their credit history, a sudden disclosure will lead to CIBIL harm. Loan Jagat explains this in a detailed manner. Read here:

https://www.loansjagat.com/blog/cibil-score-mistake-to-avoid

Disclosure of credit cards often results in shortening the account history, which the bank will never see, even if you have performed so well. So, when it comes to future loans, congratulations! You have successfully made banks reject you. This is a very clean mistake that people do not realise early; they only realise it when their credit history is evaluated by credit bureaus and their CIBIL score comes below 690.

This is the major reason why early disclosure of credit cards is not a new trend but a new dent in your financial health.

Conclusion

Mistakes with credit cards are not a new thing; even smart people make them. But how these mistakes are handled in early realisation and avoided in the future is the main protagonist of the story. Always make sure not to follow these mistakes to hamper your CIBIL score, which will affect your future loans and definitely your financial health too.